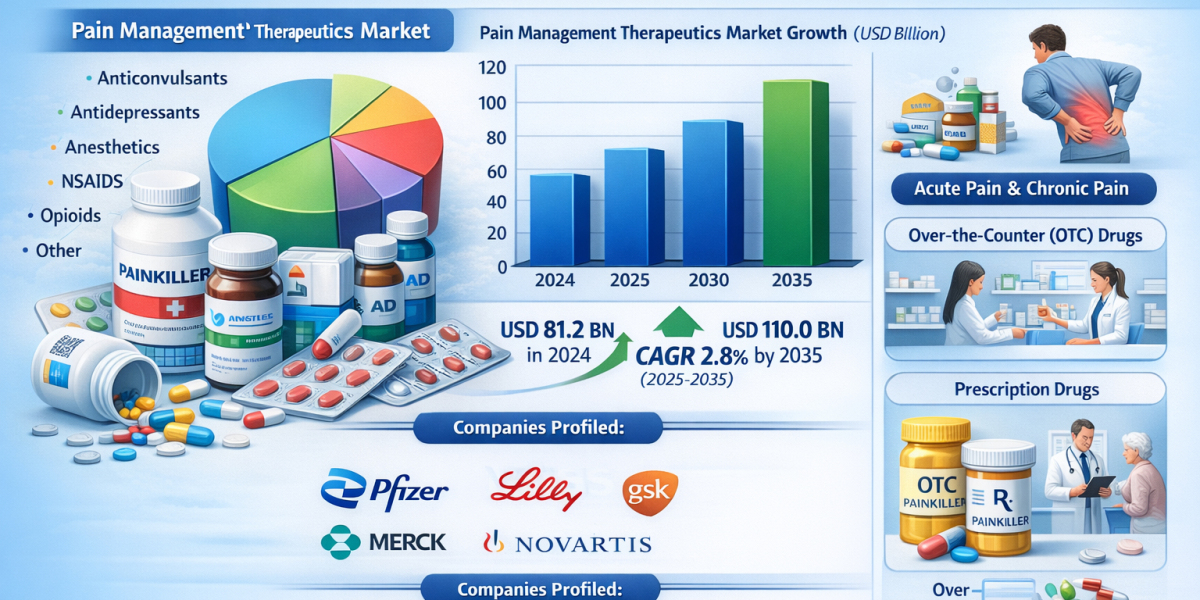

The global Pain Management Therapeutics Market was valued at USD 81.2 billion in 2024 and is projected to surpass USD 110.0 billion by 2035. The market is expected to grow at a CAGR of 2.8% from 2025 to 2035, supported by the rising prevalence of chronic pain conditions, an aging global population, increasing surgical procedures, and continued demand for both pharmacological and non-opioid pain management therapies.

Dive Deeper into Data: Get Your In-Depth Sample Now! https://www.transparencymarketresearch.com/sample/sample.php?flag=S&rep_id=1059

The pain management therapeutics market is poised for steady growth, owing to increasing prevalence of chronic pain conditions including arthritis, neuropathic pain, and pain related to cancer – particularly in aging population. North America has the most advanced market due to it being home to established healthcare delivery systems and significant chronic pain burden on the healthcare system.

Key Findings of the Market Report

- Pharmacological Products continue to dominate the sector, contributing approximately 68.9% of total revenue in 2026. Within this, Opioids still hold the largest share (~37.4%–47.9%) due to their efficacy in severe cancer and surgical pain, though their growth is slowing relative to alternatives.

- NSAIDs (Non-steroidal Anti-inflammatory Drugs) remain the leading non-opioid segment, favored for their accessibility and high use in treating arthritis and mild-to-moderate musculoskeletal pain.

- Neuropathic Pain is the fastest-growing indication segment, fueled by the rising global prevalence of diabetes-related peripheral neuropathy and post-herpetic neuralgia.

- Retail Pharmacies lead distribution with a 51.9% share, driven by high OTC demand and the convenience of repeat prescriptions for chronic conditions.

- North America remains the largest region (holding ~36%–42.6% share), while Asia-Pacific is the fastest-growing market due to rapid healthcare modernization and a massive geriatric patient pool in China and Japan.

Global Pain Management: Growth Drivers

- Breakthrough Non-Opioid Approvals: 2025/2026 marks the arrival of Nav1.8 inhibitors (e.g., Vertex’s suzetrigine/Journavx). These "blockbuster" candidates offer the efficacy of opioids without the central nervous system side effects or addiction risk, fundamentally changing the standard of care for acute pain.

- Aging Global Population: Chronic pain conditions such as osteoarthritis and degenerative disc disease are increasing. It is estimated that 1 in 4 adults globally will be over 60 by 2030, a demographic that utilizes pain therapeutics at 3x the rate of younger cohorts.

- Multimodal Pain Management: There is a strong clinical shift toward "stacking" different drug classes (e.g., an anticonvulsant with a topical lidocaine patch) and non-drug therapies to provide superior relief with lower individual drug doses.

- Regenerative Medicine: Platelet-Rich Plasma (PRP) and stem-cell-based therapies are moving from experimental to mainstream for joint and soft tissue pain, targeting the source of the pain rather than just masking the symptom.

Global Pain Management: Regional Landscape

- North America: The value leader. Growth is driven by the rapid transition to premium non-opioid biologics and a robust regulatory environment that incentivizes abuse-deterrent formulations.

- Europe: Heavily focused on Biosimilars and Generics. As major patents for branded pain meds expire, European markets are leading in the adoption of cost-effective alternatives to sustain public healthcare budgets.

- Asia-Pacific: The volume engine. Increasing disposable income and expanding insurance coverage in India and China are providing millions of new patients with access to modern pain management for the first time.

Global Pain Management: Key Players

The market is a battlefield between traditional pharma giants and biotech innovators focused on "opioid-sparing" solutions.

- Pfizer Inc. (Leader in neuropathic pain with Lyrica and biosimilar portfolios)

- Johnson & Johnson (Dominant in both pharmaceutical and surgical pain devices)

- Novartis AG (Focused on high-end adjuvant analgesics and gene therapies)

- Bayer AG (Global leader in the NSAID segment with Aspirin and Aleve)

- Eli Lilly and Company (Leader in anti-migraine biologics like Emgality)

- Vertex Pharmaceuticals (Pioneer of the NaV1.8 inhibitor class)

- Teva Pharmaceutical Industries Ltd. (World leader in generic pain medications)

- Endo International plc

- AbbVie Inc. (Allergan)

- GlaxoSmithKline (GSK)

Recent Developments (2025–2026)

- January 2026: Vertex Pharmaceuticals confirmed the successful commercial rollout of Journavx (suzetrigine), which is already being integrated into standard postoperative protocols in over 400 U.S. hospitals.

- February 2026: Medtronic received updated FDA clearance for its AI-integrated spinal cord stimulators that use closed-loop sensing to adjust electrical impulses based on real-time nerve signals.

- December 2025: Endo International expanded its generic portfolio with the launch of several "abuse-deterrent" opioid formulations, aimed at meeting new stringent safety mandates.

Buy this Premium Research Report: https://www.transparencymarketresearch.com/checkout.php?rep_id=1059<ype=S

Global Pain Management: Segmentation

By Drug Class

- Opioids (Volume leader; declining growth)

- NSAIDs (Non-steroidal Anti-inflammatory Drugs)

- Anticonvulsants & Antidepressants (For Neuropathic pain)

- Anesthetics (Local & Regional)

- Anti-Migraine Agents (Triptans & CGRPs)

By Indication

- Chronic Pain (Arthritis, Back Pain) — (Largest Segment)

- Neuropathic Pain — (Fastest Growing)

- Cancer Pain

- Acute/Post-Operative Pain

By Distribution Channel

- Retail Pharmacies (51.9% share)

- Hospital Pharmacies

- Online Pharmacies (Fastest growing channel; 9.4% CAGR)

About Transparency Market Research

Transparency Market Research, a global market research company registered at Wilmington, Delaware, United States, provides custom research and consulting services. Our exclusive blend of quantitative forecasting and trends analysis provides forward-looking insights for thousands of decision makers. Our experienced team of Analysts, Researchers, and Consultants use proprietary data sources and various tools & techniques to gather and analyses information.

Our data repository is continuously updated and revised by a team of research experts, so that it always reflects the latest trends and information. With a broad research and analysis capability, Transparency Market Research employs rigorous primary and secondary research techniques in developing distinctive data sets and research material for business reports.

Contact:

Transparency Market Research Inc.

CORPORATE HEADQUARTER DOWNTOWN,

1000 N. West Street,

Suite 1200, Wilmington, Delaware 19801 USA

Tel: +1-518-618-1030

USA – Canada Toll Free: 866-552-3453

Website: https://www.transparencymarketresearch.com

Email: sales@transparencymarketresearch.com